Advice is loud when the person giving it has something to gain – and the financial services industry has a lot to gain by convincing you that the best place for your money is in their hands. To be fair, there can be value in the services of some financial advisors. But the other side of this story needs to be told: there are many advantages DIY investors have over the pros.

Investors often start managing their own money reluctantly, feeling like underdogs. But has it ever occurred to you that DIY investors may actually have the advantage? In fact, behavioral finance has shone a light on numerous ways in which professionals, often through no fault of their own, are set-up for failure when it comes to growing the wealth of their clients.

With a little knowledge and interest in personal finance, individual investors can, and do, beat the pros. It happens all the time; you don’t hear about it because, unlike the financial services industry, most of us don’t have anything to gain by spreading that message. It’s not luck, nor is it access to some secret tome of investment knowledge. A major factor in our success is that DIY investors simply don’t have to deal with the same fees, culture, and constraints that the pros do.

Here are ten reasons why managing your own money will often beat the pros.

1. Save on fees

We’ve heard it a million times before, but even deceptively small fees have a massive negative impact on wealth. Investing $100k at 7% for 35 years will result in a tidy nest egg of almost $1.1 million. Tacking on an annual 2% fee might not sound like much, but would effectively cut your final balance in half. Financial services represent a 63 billion dollar industry in Canada – 63 billion dollars from fees of various forms. There are a lot of well-meaning people working in it, but the fact is that the industry is built upon increasing their wealth, not yours. Saving fees by investing your own money might be the most important financial decision you can make.

2. Choose investments based on appropriateness rather than compensation

Because the vast majority of financial advisors in Canada are compensated based on the investments they select for their clients rather than by their clients directly, what is best for the investor is frequently at odds with what is best for the advisor. Put yourself in their shoes: as an advisor, would you suggest the broad-based mutual fund that will kick back a generous fee into your account, or the index fund that will pay you nothing but accomplish the same goal for the client and save them tens of thousands of dollars? The incentives of paid professionals can never be truly aligned with the investor.

3. No one knows your values like you do

Aligning incentives with financial goals is essential, but understanding those goals is even more important. Having a lot of money is not a worthy goal in itself; it is what can be accomplished with that money that is important. This is about values. The financial services industry is a construct of capitalism – it values profit above all else. You may like the feeling of financial security, but I would bet that other values are equally or even more important to you: family, community, personal development, philanthropy, etc. Money is a tool that can help you create the life you want to live. Why paint the picture of your life by paying someone else to hold the brush for you?

4. Tune out the noise

Professionals are constantly exposed to a barrage of investment information. The signal to noise ratio from the firehose of daily news is vanishingly small, while the cognitive toll is high. They are compelled to pay attention to short term volatility which triggers the most destructive behavioural errors. DIY investors, on the other hand, have the luxury of tuning out the noise, developing a sound long term strategy, setting it in motion, and checking our portfolios only when appropriate – perhaps every six to twelve months.

5. Peer pressure

Because of their compensation structure, professional money managers are always comparing their actions and performance to that of their peers. Strategies that are popular but risky are overused (a factor in the growth of bubbles), while those that are sound but unpopular are under-utilized. There are enormous incentives to stick with the herd, hence the most popular mutual funds are essentially closet index funds with high fees. DIY investors need not be influenced by such financial peer pressure.

6. True long term outlook

We all know that it’s the long term that matters, but professionals are hamstrung by a culture that prioritizes short term outcomes over long term goals. Compensation models are built on quarterly and annual metrics so there is enormous pressure to abandon sound investing principles if they are temporarily underperforming. Furthermore, professional money management is an intensely competitive environment. Even if compensation is not directly tied to short term outcomes, the optics of short term inferior performance relative to one’s peers is an intolerable position – even if it is in the best interests of investors. DIY investors face no such issues and are free to focus on what matters: long term performance.

7. It’s okay to do nothing

Over-activity is the enemy of performance; not only does frequent trading rack up fees, it often has negative tax implications and, most importantly, exposes the investor to more situations in which to fall prey to behavioural errors. There are three reasons professional investors fall prey to over-activity: first, they are compelled to act by constant awareness of market volatility and financial news-feeds; second, inactivity may be misconstrued as incompetence by peers and superiors; third, it is difficult to justify high fees by doing less, even when it is the right thing to do. DIY investors, on the other hand, have the liberating ability to make evidence-based long term investment decisions, then leave those accounts alone. As Buffet has said, “The stock market is designed to transfer money from the active to the patient.”

8. Benchmark blindness

Comparing portfolio performance to a benchmark is one of the most popular ways to gauge the ability of a professional investor, but this practice carries significant behavioural risks. By focusing on short term outcomes rather than a sound investing process, all kinds of behavioural errors come into play. Decisions are driven not by logic and evidence, but a myopic obsession with short term comparisons. DIY investors need not be concerned with such benchmarks and are free to focus on process rather than outcomes.

9. Time horizon clarity

Time horizons are an important factor when creating a financial plan, and are relatively simple for the individual investor; are you planning for a twenty year retirement? Thirty? Forty? It is not so simple for professional investors. Are investment decisions made based on quarterly performance reviews? Annual fee targets? The three year minimum assessment window for professional fund managers? Conflicting time horizons compromises good decision making. All of us are susceptible to short-term thinking, but professional investors are especially vulnerable.

10. It doesn’t have to look good to anyone else

If you’re starting to get a sense of how difficult it is for professional investors to make good decisions, you’re on the right track. Here’s one more subtle but important point: It is far easier to sell a portfolio if it contains long term winners – even if the fund hasn’t held those winners for very long. This is one reason professional investors often sell out of underperforming assets (sell low) and buy into hot stocks (buy high). When you are forced to consider the optics of your behaviour, it is often easier to justify conformity and failure than unpopular positions with a higher chance of success. The portfolios of DIY investors only have to look good to themselves.

Conclusions

Whether you are a professional or amateur, investing is rife with behavioural pitfalls. But there is no reason to believe that successful DIY investors are lucky or the exception to the rule. In fact, there are numerous structural reasons inherent in the financial services industry that put professional investors at a disadvantage to DIY investors. These largely revolve around fees, short-term thinking and overactivity.

There are many investment styles that DIY investors have used successfully. The one I have used and now write about on this blog is based on dividend investing using the Beating the TSX strategy. This is a simple system anyone can use to build a no-fee, low-maintenance portfolio of large Canadian dividend paying stocks. Over the last thirty years it has out-performed the index by 2-3% annually (on average), with minimal annual updating.

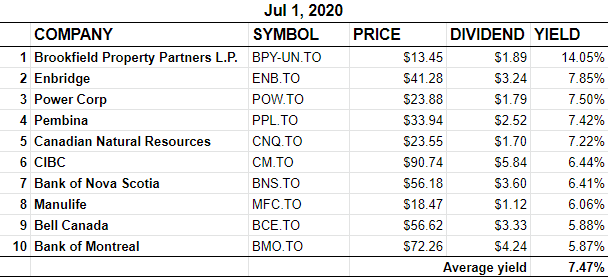

Here is the current BTSX portfolio:

When I was researching for this post, I came across a few articles that covered similar material and really helped with the content: this great post by Joe Wiggins at behaviouralinvestment.com and this article by Barry Ritholtz. Thanks, gentlemen.

{kind=link}

Hello Matt. Thank-you for your continuing education work and updates to a good investing strategy. Our investing process incorporated many of your DIY insights.

The benefits of quality companies with good yields and dividends reinvested in the accumulation stage can be truly remarkable. Thirty years ago we bought our first company ; 100 shares of Bank of Nova Scotia. With dividend reinvestment and share splits we accumulated over 1300 shares and our initial investment is more than returned every 6 months via dividends. The process worked incredibly well and is a substantial supplement to our retirement funds. One must choose quality companies with good yields, a discernible future and some dividend growth. Over the years we also acquired many of the companies on your lists.(BCE,TRP, ENB,T, FTS, CU and EMA….) The only stinker was TransAlta Utilities which basically returned our capital after many years. Regards Mike

Thanks for sharing your story, Mike. It can be hard for people to resist the sales pitch of the financial services industry, but the long term benefits of a simple dividend-based strategy are really amazing, and your situation illustrates this well.

(And don’t sweat TransAlta – every good strategy has a few soft spots; we have to put up with them to reap the larger rewards)

Good afternoon Matt, Good to read your comments on DIY investing ! Like Mike his portfolio of stocks is similar to ours, and we could add most of the banks which have done well. Always enjoy following Beating the TSX Strategy In The Moneysaver which we have enjoyed for many years!! Keep up the good work, Herb

I always read with great interest. Important for investors that we look beyond Covid and not let emotions take over.

Pingback: Using BTSX to build your portfolio: a step by step guide —